The concept of Farmer Producer Company or Producer Company has its roots in the Companies Act, of 1956. It is one of the few provisions of the Companies Act of 1956 that has been retained as it is in the Companies Act of 2013. Also known as Farmer Producer Organisations (FPO), these companies are formed to carry out activities related to agriculture. Similar to other types of companies, a Producer company also has to comply with the provisions of the Companies Act, 2013 regarding annual filing. This blog highlights the Annual Compliances of Farmer Producer Company along with the benefits of doing so and the consequences of non-compliance.

What is a Producer Company?

A Producer Company (PC) is a new legal company that exclusively contains particular types of people, such as agricultural production, forest produce, artisan items, or any other local produce, and whose members are primary producers. It was established as a legal entity in 2003 under Section IX-A of the Indian Companies Act 1956.

Definition as per Companies Act, 2013

As per Section 378A(l) of the Companies Act, 2013, a Producer Company means a body corporate that has its objects or carries out activities that are laid out in Section 378B and which is registered as a Producer Company under the Companies Act, 2013 or Companies Act, 1956.

Mandatory Annual Compliances of farmer producer company

A Producer Company is mainly governed by the Companies Act of 2013. However, being a company, it also has to comply with the Income Tax Act of 1961. In light of this, the following are the mandatory annual compliances of a Producer Company.

Companies Act, 2013

Following are the mandatory annual compliances of a Producer Company as per Companies Act, 2013.

Annual General Meeting (AGM)

It is mandatory for every company registered under the Companies Act, 2013, except an OPC, to hold an annual general meeting every year. It shall be held within six months from the end of the financial year. However, the gap between the two AGMs cannot be more than 15 months. Also, the first AGM of a producer company shall be held within 90 days from the date of its incorporation.

The Notice for the general meeting shall be in writing and shall be given at least 14 days prior to the meeting. Along with the notice, attach the agenda of the meeting, minutes of the previous general meeting, financial statements and report of the Board of Directors, and names of candidates who are qualified to become directors for election.

In addition, if the members of the Producer Company are individuals, they shall be entitled to a single vote in the general meeting irrespective of the shares held by them in the company. Further, the quorum i.e., the minimum number of members required for a valid meeting, shall be 1/4th of the total number of members, unless the articles provide for a higher number.

Board Meetings

According to the provisions of the Companies Act, 2013 regarding Producer Companies, a minimum 4 board meetings shall be held every year. Also, at least 1 meeting shall be held every 3 months. The quorum for such meetings shall be 1/3rd of the total number of directors or 3 directors, whichever is higher.

Director’s Report

It is necessary for every company to attach to its financial statements a report by the Board of Directors of the company. It shall contain particulars as specified in Section 134 of the Companies Act, 2013.

General Reserve

A Producer Company shall maintain a general reserve each year. In case of insufficient funds for transfer to the reserve, the members of the Producer Company shall contribute the same in accordance with their share in the company.

Internal Audit

As per the provisions of the Companies Act, 2013, an internal audit of a Producer Company is mandatory. It shall be done by a Chartered Accountant at such interval and in such manner as specified in articles of the company.

Further, a Producer Company shall file the following forms and returns.

| S. No | Form Type/ Purpose | Form No. | Due Date |

| 1. | Annual Financial Statements | AOC – 4 | Within 30 days of holding of Annual General Meeting |

| 2. | Annual Return | MGT – 7A (For Small Companies) MGT – 7 (For Other Companies) | Within 60 days of holding of Annual General Meeting or the due date of the Annual General Meeting, whichever is earlier |

| 3. | Disclosure of Interest by the Director to the Company | MBP – 1 | In the First Board Meeting of each Financial Year |

| 4. | Disclosure of Non-Disqualification by the Director to the Company | DIR – 8 | In the First Board Meeting of each Financial Year |

| 5. | Director KYC | DIR – 3 KYC | 30th September of each year |

| 6. | Return of Deposits – For sums not to be considered as deposits as of 31st March | DPT – 3 | 30th June of each year |

| 7. | Appointment of Auditor, if any | ADT – 1 | Within 15 days from the Annual General Meeting in which Auditor is appointed |

| 8. | Statement of Unpaid and Unclaimed Amounts | IEPF – 2 | Within 60 days of holding of Annual General Meeting or the due date of the Annual General Meeting, whichever is earlier |

| 9. | Disclosure of Significant Beneficial Owner | BEN – 2 | Within 30 days from receipt of BEN-1 from the shareholder |

| 10. | Pending payment to Vendors in case of MSME | MSME – 1 | As it is a half-yearly return, the following are the due dates – For 1st April to 30th September – 30th October For 1st October to 31st March – 30th April |

Income Tax Act, 1961

As per Section 2(31) of the Income Tax Act, 1961, a person includes a company. Therefore, a Producer Company shall file the return of its income on an annual basis.

| S. No | Form Type/ Purpose | Form No. | Due Date |

| 1. | Income Tax Return | ITR 6 | 31st October of the assessment year |

Want to avoid the last-minute hassle? Connect with us and file the income tax return of your company now!

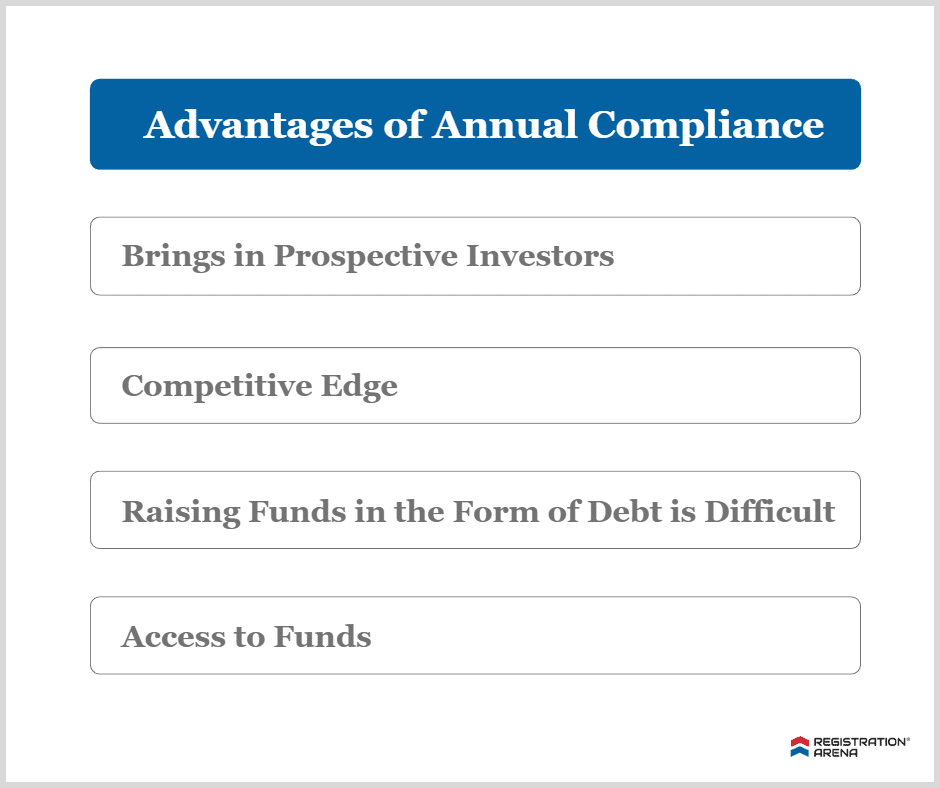

Advantages of Annual Compliance

Following are the advantages of annual compliance to a Producer Company.

Brings in Prospective Investors

Before investing in any company, investors often review its financial statements and legal compliance status. Therefore, if a producer company complies with the law well on time, it helps in attracting investors.

Competitive Edge

Compliance with the law gives a company a competitive edge in the market. Therefore, annual compliance can help a producer company in attracting new customers and retaining the existing ones.

Active Status

If a company fails to file annual returns or forms as specified in the Companies Act, 2013, the Registrar of Companies (ROC) strikes off its name from the Register of Companies. Therefore, annual compliance helps a Producer Company in maintaining its active status.

Access to Funds

Consistency in fulfilling compliance requirements is used to assess the credibility of the company. Therefore, annual compliance makes access to funds easy for a producer company.

Consequences of Non-Compliance

The following are the consequences of non-compliance by the Producer Company-

Payment of Additional Filing Fees

In case a company fails to file forms on or before the due date, it has to pay additional filing fees to the ROC. For example, if AOC-4 or MGT-7 are not filed on time, then a company has to pay additional fees of Rs. 100 per day.

Penalty on Company and its Officers

In case of default in annual compliance, a penalty is also levied on the company and the officers who are in default. For instance, if AOC-4 or MGT-7 are not filed on time, then the company and its officers are liable to a penalty of Rs. 10,000, and a further penalty of Rs. 100 per day, which can go up to Rs. 2,00,000 in case of the company and Rs. 50,000 in case of officers in default.

If form ITR-6 is filed after the due date i.e., 31st October, a penalty of Rs. 5000 is levied in case the income of the company exceeds Rs. 5 lakhs. In case the income of a company does not exceed Rs, 5 lakhs, a penalty of Rs. 1000 is levied.

Disqualification of Directors

If a company fails to file its financial statements (AOC-4) or annual return (MGT-7) for a continuous period of 3 financial years, then its directors become disqualified. They can neither be reappointed in the same company nor be appointed in another company for 5 years after such failure.

Inactive Company

If a company fails to file its financial statements (AOC-4) or annual return (MGT-7) for a continuous period of 2 financial years, then ROC declares it as an inactive company, and its name is stricken off from the register of companies after a notice is served.

Audit of Producer Company

Similar to other companies, a Producer Company is subject to audit under the following acts.

Companies Act, 2013

Accounts of all the companies registered under the Companies Act, 2013 shall be audited by a Chartered Accountant or a firm of Chartered Accountants. Therefore, an audit is mandatory for a producer company as well.

Income Tax Act, 1961

Section 44AB of the Income Tax Act, 1961 provides for a mandatory tax audit of a company (including Producer Company) in the following cases.

In the case of Business

If the company carries on a business and turnover exceeds Rs. 1 crore. However, if cash transactions are up to 5% of gross receipts or payments, then an audit is required only if the turnover exceeds Rs. 10 crores.

In the case of the Profession

If the company provides professional services and turnover exceeds Rs. 50 lakhs.

Further, if a tax audit is mandatory for a company, then it shall file an audit report on or before 30th September every year.

Conclusion

The concept of a Producer Company is beneficial for farmers if they want to carry out business in an organized form. However, annual compliance is necessary to be it any type of company as it offers several advantages. Registration Arena has a professional team who can assist you in the registration of your business as well as compliance with regulatory requirements.

Call us now at +918600544411/22 or drop an email at sales@registrationarena.com for more information.