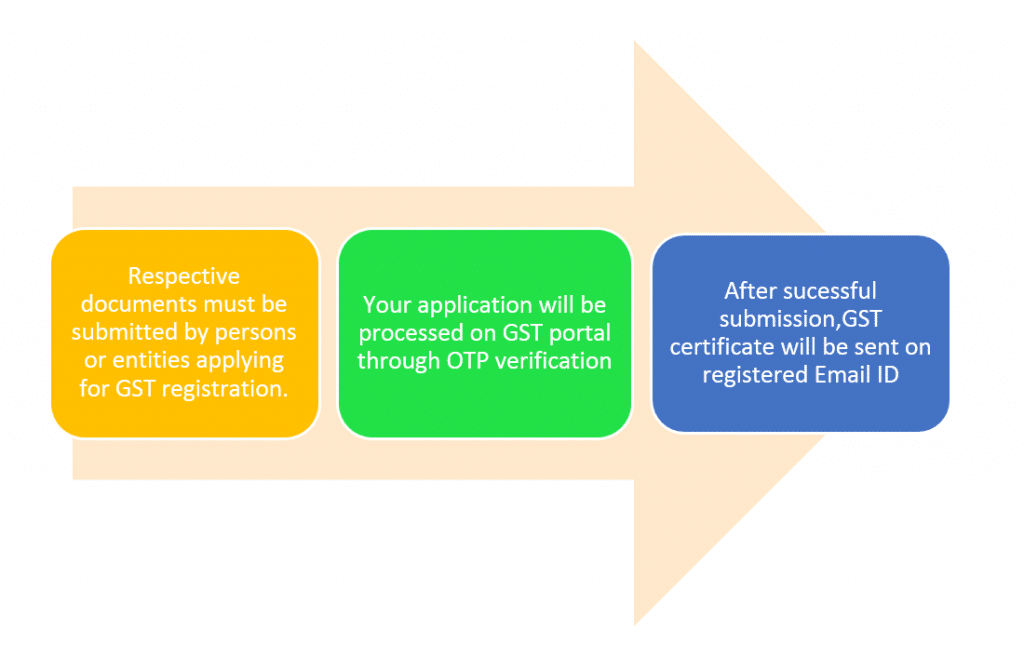

GST REGISTRATION

GST is said to be one of the biggest tax reform in India. GST registration has helped in the improvement of business and increasing tax payer base by bringing up all the small businesses in India. It has converted all the multiple taxes that we have to pay into a single system. The tax complexities have reduced while the tax base is increased. Under the new GST, all entities involved in buying or selling goods and services (subject to turnover limit) are required to register for GST. Any entity without GST registration will not be allowed to collect GST from the customers or claim any input tax credit of GST paid and/ or could be penalised. Furthermore, GST registration is mandatory once an entity crosses the minimum threshold turnover of its new business that it expected to cross.

GST TURNOVER LIMIT

There are many types of GST registration and some types of entities like casual taxable persons, non-resident taxable persons or persons supplying through E-Commerce operators are required to mandatorily obtain GST registration irrespective of the turnover limit. The GST turnover limit for regular GST for goods and service providers is given below:

Service Providers: An entity which provides services for more than Rs.20 lakhs in aggregate turnover in a year is required to obtain a GST registration in special category states, the GST turnover limit for service providers has been fixed at Rs.10 lakhs.

Goods Suppliers: A person who is engaged in exclusive supply of goods whose aggregate turnover crosses Rs.40 lakhs in a year is required to obtain GST registration. To be eligible for the Rs.40 lakhs turnover limit, the supplier must satisfy the following conditions:

- The supplier should not be providing any kind of services.

- The supplier should not be engaged in making intra-state (supplying goods within the same state) supplies in the States of Kerala, Telangana, Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland, Pondicherry, Sikkim, Tripura and Uttarakhand.

- The supplier should not be involved in the supply of ice-cream, pan masala or tobacco.

If the above given conditions do not meet, then the supplier of goods would be required to obtain GST registration when the turnover crosses Rs.20 lakhs and Rs.10 lakhs in special category states.

Special Category States: Under GST, the following are listed as special category states – Arunachal Pradesh, Assam, Jammu and Kashmir, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Himachal Pradesh and Uttarakhand.

Aggregate Turnover: Aggregate turnover = (Taxable supplies + Exempt Supplies + Exports + Inter-State Supplies) – (Taxes + Value of Inward Supplies + Value of Supplies Taxable under Reverse Charge + Value of Non-Taxable Supplies).

The Aggregate turnover is calculated based on the PAN. Hence, even if one person has multiple places of business, it must be summed to arrive at the aggregate turnover.

GST REGISTRATION RESPONSIBILITIES AND COMPLIANCE

There are various responsibilities and compliance to take care of under GST registration from time to time. Failure to comply with the GST regulations or compliance requirements can lead to penalties and revocation of GST registration by the authorities. Some of the main responsibilities of a person registered under GST include:

- Collecting and remitting GST amount from the customers.

- Issuing the proper GST invoice as per the GST rules and regulations.

- Filing of the GST returns whenever required based on the turnover – if there is no turnover or business activity.

- Filing of the GST annual return.

Maintaining all the records pertaining to GST for the periods of 8 years.